Making Carbon Removal Work for Europe:

A Scale-Up Strategy for 2026–2030

Executive Summary

Permanent carbon removals (CDR) are essential for industrial competitiveness and climate policy. Hard-to-abate sectors such as steel, cement, chemicals and glass will require them to counterbalance residual emissions. At scale, CDR will safeguard the integrity of the EU ETS, create new jobs, and strengthen the EU’s export-oriented clean-tech value chains.

Scaling novel CDR capacity to the EU’s ambition of five million tonnes by 2030 will require a strategic approach. A combination of demand stimulus, technology deployment support, and policies will be needed to mobilise purchases and investment and strengthen market confidence in durable carbon removals. This note sets out an industry assessment of the policy action required and proposes a model strategy to achieve this objective (1). The challenge is urgent. Europe’s question is not whether CDR will be needed, nor whether sufficient projects exist. It is whether policy can create enough demand, funding, and certainty to turn today’s project pipeline into operating capacity over the next years. Projects must secure offtakes and financing starting now if sufficient supply is to be available when compliance demand emerges.

To address this challenge, this paper proposes a model strategy for the period 2026-2030 to:

Create early demand through an EU Buyers’ Club to expedite buyer engagement and learning and a Purchasing Facility to provide price support and risk-sharing in offtakes.

Mobilise deployment funding through EU programmes and ETS revenues (Innovation Fund, Industrial Decarbonisation Bank) to reduce risks and accelerate investments.

Strengthen research and innovation through dedicated support under the European Innovation Council and Framework Programme 10.

Provide regulatory certainty by accelerating CRCF methodology development, clarifying use cases for CDR credits, and establishing regulatory sandboxes for emerging pathways.

Build the foundations by developing the governance and practical experience needed for the future integration of removals into compliance markets

This Is a Make-or-Break Moment for Europe

Carbon Removal Matters for Industries, Jobs, and the Climate.

Carbon removal is essential for achieving net zero. Alongside emissions reductions, the EU will need large-scale permanent removals to address residual fossil emissions and meet its climate targets. The European Commission projects a need of around 400 MtCO₂ by 2040 to meet its 90% net reduction target, including at least 75 MtCO₂ of permanent removals by 2040, (2) when emission allowances are expected to approach zero. Permanent removals are critical to maintaining industrial growth and the integrity of the Emissions Trading System (ETS).

Carbon removal is essential for industrial growth. Hard-to-abate sectors such as steel, cement, chemicals and glass will continue to face residual emissions after abatement. Permanent removals offer a strategic hedge against rising carbon costs in the 2030s. EU ETS prices could reach €200/tCO₂ by 2035.3 Projected cost reductions across a portfolio of methods could bring the price for a blended tonne of permanently removed carbon down to around €140/tCO₂ over the same period (4). Investing early in carbon removal capacity can help limit decarbonisation costs and re-invest in new industrial processes.

Carbon removal represents a major strategic clean-tech opportunity. The EU already hosts 148 active carbon removal projects across land-, ocean-, and geologic-based pathways.(5) By 2035, the sector is estimated to create 180,000 jobs across manufacturing, transport, storage, and digital services(6). As global demand for durable removals grows in line with net-zero commitments, the market is estimated to reach a scale of up to $1.2 trillion by 2050 (7). By scaling CDR now, the EU can secure a competitive edge in the technologies and services that other economies will require to address emissions and meet climate targets.

The EU Needs a Strategic Approach to Scale Carbon Removal.

The EU aims to reach at least 5 million tonnes of permanent removals annually by 2030 up from around 0.6 million tonnes today (8). Achieving this will require up to an estimated €6 billion in EU funding for deployment support by 2030(9). Separately, an estimated €2.6 billion will be needed for research and innovation in the next EU budget (2028-2034)(10). Yet permanent CDR has received only around €0.3 billion (or 0.1% of EU funding) to date and remains largely absent from major funding programmes. (11)

Early public support is essential because current carbon market prices do not yet reward permanent carbon removals. High-integrity removal credits currently trade between €150-800 per tonne due to both the additional benefit they provide beyond abatement and the significant upfront investments required to develop projects and infrastructure. The EU must therefore help create early markets, reduce investment risks, and accelerate costs curves so that high-integrity removals become available at scale and affordable when industry needs them. This also means ETS revenues should play a central role in funding CDR. This would allow those companies paying into the ETS to benefit from the carbon removal solutions funded by ETS revenues. (12)

The EU Must Boost CDR Now.

CDR scale up is essential now—delay will increase future costs. The core challenge is that the existing project pipeline secures offtakes, financing, permits and reaches final investment decision (FID). FID taken in 2027 may deliver removals by 2030. Policy must now incentivise purchases and investments in CDR. It must scale supply to bring projects online before compliance demand bites.

The EU currently risks investing too little and too late. Failure to scale carbon removal capacity will leave EU industry with too few options to manage emissions and greater transition risks in the 2030s. Recent modelling suggests that carbon removals can act as a strategic safety valve, helping contain compliance costs while preserving the integrity of the EU ETS. (13) Without timely action, the EU risks growing pressure on industries, jobs, and the wider economy. It would lose talent and become increasingly dependent on the know- how and services supplied by other regions.

The EU therefore needs a policy mix. It should support a broad portfolio of land-, ocean-, and geologic-based removal pathways to avoid technological lock-in, maximise environmental and industrial benefits, and allow a broadest possible set of countries and sectors to engage in and benefit from CDR. At the same time, it must combine demand-pull and supply-push measures. It must both reduce technology costs and stimulate purchases by early public and private buyers. Combined EU funding across programmes should be commensurate with the scale of the challenge.

Scaling Up Carbon Removal: A Model Strategy for 2026-2030

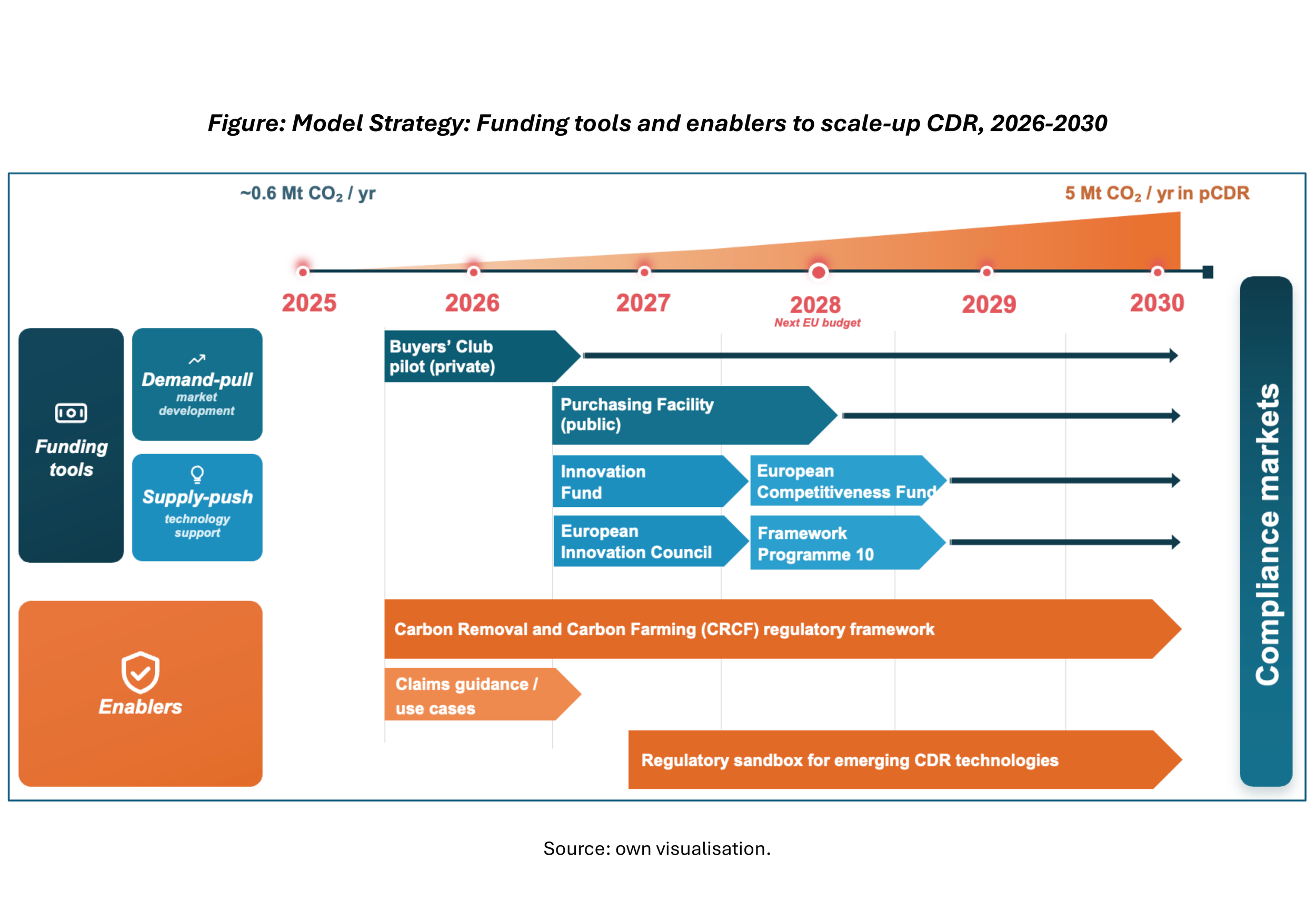

Scaling permanent carbon removal will require coordinated action by policymakers, industry, and investors over the coming years. Public policy must stimulate demand and investment across a diversified portfolio of permanent CDR methods if the EU is to reach its objective of at least 5 million tonnes of removals annually by 2030 and prepare for the integration of CDR into the EU ETS. This chapter sets out a model strategy combining targeted EU funding tools that mobilise purchasing commitments and investment with enabling policies that reduce barriers and strengthen market confidence. Together, these measures aim to build the CDR pipeline needed for EU industrial and climate policy after 2030. (14)

a. Funding Tools

2026 — EU Buyers’ Club

The EU should promote the new Buyers’ Club in 2026 to aggregate demand, standardise contracting, and lower transaction costs for durable carbon removals(15). The Buyers’ Club should support purchases across a broad portfolio of permanent CDR methods and bring new public and private buyers into the market early. It should prioritise industrial sectors expected to require removals in the future, including steel, cement, chemicals, aviation, and power generation.

The Buyers’ Club should support methods already covered under the CRCF as well as pathways under active methodology development. By reducing market-entry barriers and improving price discovery, it can help accelerate voluntary carbon markets ahead of future compliance demand and strengthen confidence among buyers and investors.16 The Buyers’ Club focuses on aggregating and facilitating demand, while a forthcoming EU Purchasing Facility should provide price support or de-risk transactions to ensure the existing project pipeline secures offtakes and commercial financing.

2027 — EU Purchasing Facility (CRCF Facility)

The EU should launch a purchasing facility from 2027 to support offtakes in permanent carbon removals through price support and de-risking mechanisms (e.g., price subsidy/contracts for difference, first-loss guarantee, buffer pool). Projects should be able to combine EU support and Member State aid through government-backed offtake agreements tied to CRCF-certified delivery. The facility should establish a multi-year plan and publish annual calls across a range of CDR methods. (17)

Funding should combine EU budget and ETS revenues, including the Innovation Fund, the European Innovation Council, and the Industrial Decarbonisation Bank (IDB). The Commission should allocate 5% of the IDB’s €100 billion envelope in 2027-2030 for CDR, commensurate with funding needs (including through the IDB’s investment booster before 2028). This would help industrial emitters access CRCF-certified removals and address residual emissions while returning value to ETS contributors through a polluter-pays mechanism. (18)

The Commission should also procure removals for its own emissions by 2030 and establish a clear pathway towards direct EU purchasing.(19) Action is needed immediately. Investment decisions taken in 2027 may only result in removals by 2030. Delaying support risks supply shortages and growing pressure on the EU ETS.

Looking ahead, the purchasing facility could evolve further to coordinate carbon removal procurement across the EU. It should allow the Commission to run “auctions-as-a-service” for Member States, centralising procurement and reducing administrative costs. In addition, the facility could evolve into a platform for coordinated procurement of international removal credits in support of the EU’s 2040 climate framework.(20).

2027–2028 — European Innovation Council and Framework Programme 10

The European Innovation Council (EIC) should introduce dedicated challenges for carbon removal technologies from 2027 onwards under both the Pathfinder and Accelerator programmes. These calls should support a broad range of permanent CDR pathways across research, innovation and demonstration stages, including but not limited to accelerated mineralisation in situ or materials, enhanced rock weathering, biomass burial, direct ocean capture and ocean alkalinity enhancement, DACCS, BECCS, biochar, as well as advanced digital technologies for monitoring, reporting and verification.(21)

Within the next EU budget (2028-2034), the Framework Programme 10 (FP10) should include a dedicated budget for permanent carbon removal research and innovation. As FP10 expands, the Commission should establish ring-fenced CDR funding and cluster CDR-specific calls. FP10 should support early-stage innovation while the European Competitiveness Fund supports commercial deployment. (22)

2027–2028 — Innovation Fund and European Competitiveness Fund

The Innovation Fund should explicitly recognise permanent CDR as a distinct net-zero technology category from 2027 onwards. Dedicated CDR calls should be introduced across all Innovation Fund windows, including large-scale, small-scale, pilot, and manufacturing streams.

Evaluation criteria should move beyond an abatement-focused framework and must reflect the full climate value of durable removals. GHG accounting should capture full carbon cycles, while cost-efficiency criteria should recognise the long-term value of negative emissions for ETS-covered industries. Funding structures should also better align with future offtake arrangements to improve project bankability.

Starting with the next EU budget (2028-2034), the European Competitiveness Fund (ECF) should explicitly include carbon removal technologies within its mandate. Recognising CDR as a net-zero technology is essential to unlock dedicated funding streams and future policy instruments, including the future establishment of an EU Removals Fund endowed with sufficient funding for dedicated deployment support across industries(23)

b. Enablers

2026–2030 — CRCF Framework

Several promising carbon removal pathways, particularly ocean- and mineral-based methods in open systems, still lack recognition under the CRCF. Without regulatory certainty, these approaches struggle to secure funding and generate the evidence needed for future methodology development. As a result, Europe risks slowing innovation and losing investment to other regions.

The Commission and the CDR Expert Group should use the upcoming reviews of the CRCF in 2026 to provide greater clarity on the pathway for the development of additional CRCF methodologies, including through either indicative timelines or criteria for initiating work on them. This should give developers and investors a clear line of sight for the recognition of the full range of permanent carbon removal pathways the EU will need. EU funding programmes and purchasing mechanisms should support both certified methods and approaches under active CRCF development to ensure that innovation is not held back by regulatory delays.

In parallel, the Commission should ensure the timely operationalisation of the EU-wide CRCF registry by the end of 2028, providing the infrastructure needed for the issuance, tracking and transparent management of certified carbon removal units.

2026 — Safe Claims / Use Cases

The Commission should provide guidance on how CRCF-certified removals can be used in voluntary and future compliance markets. Market participants should receive certainty on how CRCF-certified removals can be used in reporting and future compliance; possibly safe- harbour protections against claims-related litigation. The Commission should consider providing guidance to Member States indicating that claims derived from CRCF-certified credits are legitimate. This is necessary to strengthen confidence and unlock purchasing commitments, including in the EU Buyers’ Club. The Commission should clarify how CRCF units can be reflected in both corporate reporting and national inventories, while providing a line-of-sight provision for their future use within the ETS.

2027–2030 — Regulatory Sandbox

The Commission should establish an EU-wide regulatory sandbox for carbon removal under the Net-Zero Europe Platform. The sandbox should support monitored field trials, data collection, and regulatory learning for emerging land- and ocean-based CDR methods. This would accelerate methodology development, improve licensing pathways, reduce uncertainty for investors, and help bring additional removal capacity online before 2030.

The EU Must Act Now for Carbon Removal to Deliver Value for Its Industries and Society

Permanent carbon removals will deliver value for both countries and companies. For governments, they help preserve the integrity of climate policy, safeguard industrial competitiveness, create new jobs in the transition to net zero economy. For companies, they offer a pathway to manage future carbon costs, secure access to scarce high-quality removals, and reduce transition risks. With the right policy framework, carbon removal can become a strategic asset for EU’s economy and climate objectives.

The challenge is to build a functioning market and sufficient capacity in time. The EU aims to increase annual permanent removal capacity from around 0.6 MtCO₂ today to at least 5 MtCO₂ by 2030. Achieving this will require both stronger demand signals and accelerated project deployment. While a pipeline of projects is under development, many lack the revenue certainty, financing, and policy clarity needed to reach final investment decision.

The next five years will be critical. Early Government-led demand signals for additional purchases as well as deployment support is needed to help bring projects to market, advance learning curves, and reduce costs through scale. Final investment decisions must be taken within the next one to two years if removals are to be delivered at scale by 2030. Without coordinated demand-pull and supply-push policies, Europe risks missing a narrow window to put permanent carbon removal on a growth trajectory aligned with its industrial and climate ambitions.

To close this gap, the EU should pursue the following priorities ahead of the 2030s:

Create early demand. Launch the EU Buyers’ Club and establish a purchasing facility that provides price support and / or risk-sharing to stimulate additional offtakes across a broad portfolio of permanent carbon removal methods.

Mobilise deployment funding. Use ETS revenues and EU budget instruments, including the Industrial Decarbonisation Bank and Innovation Fund, to reduce risks and accelerate uptake and deployment of CDR across industries.

Strengthen research and innovation. Introduce dedicated carbon removal challenges under the European Innovation Council and provide ring-fenced support under the forthcoming Framework Programme 10 (next EU budget).

Expedite regulatory certainty. Accelerate methodology development, provide guidance on the use cases of removals in voluntary and future compliance markets, and establish a regulatory sandbox for pre-CRCF CDR pathways.

Build the foundations. Develop the institutional capacity and practical experience, e.g. by establishing the purchasing facility ahead of time, to effectively integrate permanent removals into the EU ETS and international carbon removal credits in the EU’s 2040 climate framework.

Whilst the EU pioneered the world’s leading carbon market, the Emissions Trading Scheme, it must now lead the scale-up of carbon removal. To remain effective on the path to net zero, that market must evolve. Carbon removals are essential to addressing residual emissions and completing a carbon market that today remains incomplete. As the most comprehensive carbon market system that integrates both emissions reductions and carbon removals, the EU can once again set a global standard. To that end, a coordinated scale-up strategy for permanent CDR will help secure Europe’s industrial base, preserve the integrity of the EU ETS, create new jobs, and strengthen EU leadership in the clean technologies required for a net-zero economy.24

About NEP

The Negative Emissions Platform (NEP) is a Brussels-based, international partnership of permanent carbon removal project and technology developers, suppliers, investors, marketplaces, and buyers.

References

1. Drawing on interviews and consultations with suppliers, buyers, technology developers, credit portfolio managers, and marketplaces across the NEP network; building on earlier recommendations for scaling CDR, EU purchasing support and funding.

2. EC, Impact assessment Report on a 2040 Climate Target, Part 2, 2024.

3. ABN Amro, Scenarios shaping EU ETS prices, 2025.

4. Based on cost estimates for BioCCS, DACCS, and biochar carbon removal; EC / Ramboll, Carbon removals in the EU, p.41.

5. EC / Ramboll, Carbon removals in the EU, 2025.

6. BCG / DVNE, Carbon Dioxide Removal Europe and Germany’s Role in Catalyzing a Trillion-Euro Industry, 2024.

7. McKinsey, Carbon removals: How to scale a new gigaton industry, 2023.

8. EC, Sustainable Carbon Cycles Communication, 2021.

9. Authors in a 2025 study commissioned by the European Commission, using cost estimates for various permanent CDR methods, estimate that the total EU funding required between 2025 and 2030 to meet the EU’s industrial removals target of 5 MtCO₂ by 2030 (annually) ranges between €2.6 and 6.1 billion on average for portfolios of lowest cost and medium TRL removal methods, respectively; EC / Ramboll, Carbon removals in the EU.

10. Carbon Gap, The MFF, the ECF, and FP10: Decoding the EU’s budget plans and what they mean for CDR, 2025.

11. EC / Ramboll, Carbon removals in the EU.

12. ESABCC, Scaling up carbon dioxide removals, 2025; NEP / AFEN / CDR.fyi, Scaling Carbon Dioxide Removal (Policy Toolkit), 2025.

13. Best, F. et al., A Safety Valve for the EU ETS Endgame: Containing Prices through Carbon Dioxide Removal, 2026.

14. NEP, A Phased Approach to Integrating Permanent Carbon Dioxide Removals in the European Union Emission Trading System, 2026.

15. EC / Ecologic, An EU purchasing programme for permanent carbon removals, 2025.

16. NEP, Making A Short-term EU Purchasing Programme Work for Permanent CDR, 2025.

17. NEP, Making A Short-term EU Purchasing Programme Work for Permanent CDR, 2025.

18. NEP, Positioning the Industrial Decarbonisation Bank for Climate and Competitiveness: Unlocking Europe’s Carbon Removal Potential, 2025.

19. EC, Progress Review of the Communication on Greening the Commission, 2025.

20. The 2040 Climate Law is in force since 7 April 2026: up to 5% international credits from 2036, Article 6-compliant, restricted to Member States, and explicitly not eligible within the ETS.

21. NEP, The Case for Dedicated CDR Calls in the European Innovation Council, 2025.

22. NEP, Policy Brief: Turning Climate Ambition Into Economic Advantage, 2026.

23. NEP, Policy Brief: Turning Climate Ambition Into Economic Advantage, 2026.

24. NEP, A Phased Approach to Integrating Permanent Carbon Dioxide Removals in the European Union Emission Trading System, 2026.