Carbon Removal Can’t Wait: Here’s How Governments Lead the Way

By Atilla Yucel and Lambrini Margariti

Carbon removal is essential for net-zero, but it won’t scale without public policy support. Around the world, governments are beginning to build the incentives and markets needed to pull carbon from the atmosphere. Here’s what we take away from those leading the way.

Imagine trying to fight a house fire with half your water hose missing. That’s the challenge climate policymakers and corporate sustainability leaders face when trying to reach net-zero emissions without scaling up carbon dioxide removal (CDR). As global temperatures continue to rise, we need to reduce emissions fast and we also need to pull more carbon out of the atmosphere.

Permanent CDR refers to methods that actively remove carbon dioxide from the air, ocean, wood residues, or biowaste and store it for centuries. From filtering air with high-tech fans to burying biochar in soil or turning carbon into stone, these approaches are no longer science fiction. Many also offer valuable co-benefits, ranging from improved soil health to enhanced livelihoods. But they remain painfully underdeveloped. To fix this, governments must act fast.

Image: This pilot plant uses renewable energy to store carbon permanently in the ocean while helping to counteract acidification. Photo courtesy of Limenet.

How fast? Globally, 6-10 gigatonnes of CO₂ removals will be needed every year by 2050 to limit global warming to 2°C. Today, we remove only 2 gigatonnes annually, mostly through forestry. Scaling up novel, permanent removal methods will require a massive leap, like going from a single pixel to full-screen resolution in 25 years’ time.

By that time, global emissions may have pushed us past that temperature threshold. Even once net-zero—a balance between emissions and removals—is achieved, removing the excess carbon already in the atmosphere will be critical to bring temperatures down.

The Challenge: A Service Without Buyers (Yet)

Despite the fanfare around net-zero pledges, novel CDR methods aren’t scaling fast enough. At the heart of the issue is the green premium: removing carbon from the atmosphere costs far more than emitting it and there’s no functioning market to close that gap.

Project developers cite a lack of capital among the most urgent barriers to growth. Investors remain cautious, deterred by unclear demand. Meanwhile, corporate buyers hesitate because of high costs making the case for durable removals hard to justify.

Without predictable revenue streams, investment remains scarce, and promising technologies—like Direct Air Capture (DACCS), Bioenergy with Carbon Capture and Storage (BECCS), Biochar, or Enhanced Rock Weathering—struggle to improve scale and cost over time.

And yet, as governments tighten climate policies and companies move toward credible climate transition plans, the demand for high-quality credits could quickly outstrip available supply, risking a crunch as early as 2030 as some suggest.

The Remedy: Policy That Leads Capacity and Markets

The good news? We’ve seen this movie before. Solar panels, offshore wind, electric vehicles: all scaled up thanks to well-crafted public policy. What’s needed now is a toolkit for CDR, tailored to the realities of early-stage clean tech. Think research grants, procurement, and price guarantees, all designed to reduce the green premium. And in doing so, policymakers also support innovation that can improve crop productivity, create local jobs, and future-proof critical industries in line with the sustainable development goals many countries prioritise.

Image: biochar facilities such as in the Philippines turn agricultural residues into permanent carbon storage, while boosting crop yields and improving farmer livelihoods. Photo courtesy of Alcom.

“Without government backing, it is currently not feasible to build projects at scale,” says Johan Börje of Stockholm Exergi, a leading district heating and carbon removal company working to deploy BECCS in Sweden.

Dr. Benjamin Sovacool, Professor of Energy Policy at the University of Sussex, echoes this point: “You need a mix of policies that do both a supply push and demand pull. You need policies that will improve the technology and policies that will pull the market for the actual carbon removal credits.”

Here’s how seven countries are starting to get it right:

Germany: Funding the Foundations of CDR Science

Germany is laying the groundwork for long-term leadership in CDR by investing in research. Its CDRterra and CDRmare programmes explore land- and ocean-based removal methods, respectively. These publicly funded programmes don’t just run lab experiments. They also explore public acceptance, governance frameworks, and environmental impacts. Research is essential for evidence-based policy. After all, carbon removal isn’t a magic fix. It must be carefully scaled and managed to avoid unintended harm to land, water, and ecosystems.

Japan: Creating Demand Through Emissions Trading

Japan is integrating carbon removal into its emissions trading system designed to meet its 2050 net-zero goal. Companies are entitled to use credits from durable CDR methods like DACCS, BECCS, and coastal approaches for up to 5% of their emissions obligations, while allowing for credit trading. By embedding CDR into its nascent compliance market, Japan created a demand signal while encouraging companies to invest across the carbon removal value chain both domestically and overseas.

India: Using Markets to Build Capacity

In a similar vein, India is advancing a compliance market through its Carbon Credit Trading Scheme. Industrial entities that outperform emissions intensity targets earn Carbon Credit Certificates, each representing one tonne of CO₂ reduced or removed, while those falling short must purchase credits to make up the gap. In addition, a voluntary mechanism that will allow non-obligated entities to register emission reduction or removal projects for credit issuance. Together, these measures aim to catalyse climate mitigation while creating a pathway for growing carbon removal capacity in India

Kenya: Laying the Foundations with Market Infrastructure

Kenya is investing in infrastructure to lay the groundwork for global carbon market participation with its planned national carbon registry, a platform to track emissions reductions and removals and manage credit transactions. Its draft carbon market regulations also foresee fiscal incentives, including a reduced tax rate to support the development of carbon projects. Notably, proceeds from projects are intended for community development. If implemented, these measures will strengthen Kenya’s market infrastructure while encouraging investments in carbon removal, too.

Sweden: Let the Best Bid Win

Sweden has taken a different route—reverse auctions. In 2024, the government allocated €3.3 billion to support BECCS projects. Companies bid for the lowest subsidy they need per tonne of CO₂ removed, and the government awards contracts to the most cost-effective proposals. It’s an elegant way to ensure public funds are spent efficiently while also scaling up a domestic carbon removal industry. The first projects are already breaking ground.

Switzerland: De-risking Deployment

Switzerland passed its Climate and Innovation Law, which enshrines net-zero by 2050 for the economy and by 2040 for the federal government, through both emissions reductions and durable removals. To back that up, the government has launched a subsidy scheme offering up to 50% cost coverage for CDR projects like BECCS and DACCS. Funds are disbursed via competitive tenders. This kind of clear policy support provides the certainty needed to unlock private capital.

United Kingdom: Providing Price Certainty

The UK, long a leader in clean tech deployment, is now adapting its renewable energy playbook to CDR. Its approach to Greenhouse Gas Removals is based on the tried-and-tested Contracts for Difference. These contracts promise developers a fixed “strike price” for every tonne of carbon they remove. If the market pays less, the government makes up the difference. If the market pays more, the developers return the surplus. This “you-know-what-you-get” model provides long-term revenue certainty—crucial for attracting investment in capital-intensive projects like Direct Air Capture.

A Playbook for Public Sector Leaders

What do these examples teach us? That there’s no silver bullet—but there is a pattern:

Ensure a portfolio approach: Supporting a diversity of CDR pathways reduces risk, unlocks co-benefits, and fosters innovation.

Start small and learn: Piloting policy innovations can be a low-risk, high-learning opportunity allowing governments to test what works before scaling.

Support supply and demand: Alongside de-risking technologies, governments can accelerate market creation by stimulating early demand.

Build for the long haul: Technologies and markets take time to mature. Multi-year funding commitments and predictable policy matter.

Align across jurisdictions: Cross-border learning and cooperation will be essential for scaling carbon removal supply chains in cost-effective ways.

Iterate through learning: Monitor outcomes, gather feedback, and evolve instruments to match maturity of technologies and market developments.

To support governments in this journey, we developed the Policy Toolkit for Scaling Carbon Dioxide Removal—a practical guide for those tasked with selecting, designing, deploying, and justifying policy support for cleantech. It addresses a growing need: many public bodies understand why carbon removal is essential, but lack clarity on how to get started.

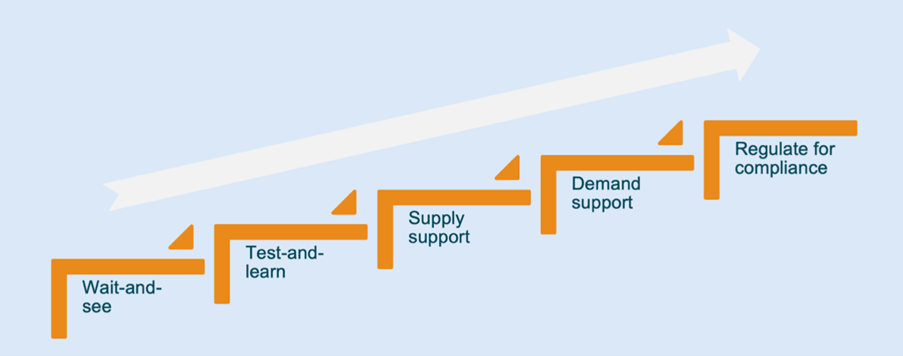

Image: Governments can scale carbon removal through a phased approach--outlined in NEP’s Policy Toolkit--that builds capacity, manages risks, and enables learning as technologies and markets mature.

The toolkit lays out a phased approach—from early exploration and test-and-learn pilots to investment support and eventual integration into compliance frameworks. For decision-makers, it’s a ready-to-use reference to build confidence, reduce risk, and steer their economies toward net-zero growth responsibly, strategically, and with public value in mind.

What’s at Stake

Getting CDR right isn’t just about hitting climate targets. It’s about creating a new clean-tech industry, generating green jobs, and securing just transitions and industrial competitiveness in a low-carbon world. One study suggests Europe alone could see up to 180,000 jobs in the CDR sector by 2035 if investment picks up.

The clock is ticking. Scaling carbon removal is essential. And—like firefighting—it requires the right tools. Those economies that stop treating carbon removal like an afterthought and start building the market now will lead the next cleantech industry.